![]()

mlforecast is a framework to perform time series forecasting using machine learning models, with the option to scale to massive amounts of data using remote clusters.

pip install mlforecast

conda install -c conda-forge mlforecast

For more detailed instructions you can refer to the installation page.

Get Started with this quick guide.

Follow this end-to-end walkthrough for best practices.

Current Python alternatives for machine learning models are slow,

inaccurate and don’t scale well. So we created a library that can be

used to forecast in production environments.

MLForecast

includes efficient feature engineering to train any machine learning

model (with fit and predict methods such as

sklearn) to fit millions of time

series.

- Fastest implementations of feature engineering for time series forecasting in Python.

- Out-of-the-box compatibility with pandas, polars, spark, dask, and ray.

- Probabilistic Forecasting with Conformal Prediction.

- Support for exogenous variables and static covariates.

- Familiar

sklearnsyntax:.fitand.predict.

Missing something? Please open an issue or write us in

📚 End to End Walkthrough: model training, evaluation and selection for multiple time series.

🔎 Probabilistic Forecasting: use Conformal Prediction to produce prediciton intervals.

👩🔬 Cross Validation: robust model’s performance evaluation.

🔌 Predict Demand Peaks: electricity load forecasting for detecting daily peaks and reducing electric bills.

📈 Transfer Learning: pretrain a model using a set of time series and then predict another one using that pretrained model.

🌡️ Distributed Training: use a Dask, Ray or Spark cluster to train models at scale.

The following provides a very basic overview, for a more detailed description see the documentation.

Store your time series in a pandas dataframe in long format, that is, each row represents an observation for a specific serie and timestamp.

from mlforecast.utils import generate_daily_series

series = generate_daily_series(

n_series=20,

max_length=100,

n_static_features=1,

static_as_categorical=False,

with_trend=True

)

series.head()| unique_id | ds | y | static_0 | |

|---|---|---|---|---|

| 0 | id_00 | 2000-01-01 | 17.519167 | 72 |

| 1 | id_00 | 2000-01-02 | 87.799695 | 72 |

| 2 | id_00 | 2000-01-03 | 177.442975 | 72 |

| 3 | id_00 | 2000-01-04 | 232.704110 | 72 |

| 4 | id_00 | 2000-01-05 | 317.510474 | 72 |

Next define your models. These can be any regressor that follows the scikit-learn API.

import lightgbm as lgb

from sklearn.linear_model import LinearRegressionmodels = [

lgb.LGBMRegressor(random_state=0, verbosity=-1),

LinearRegression(),

]Now instantiate an

MLForecast

object with the models and the features that you want to use. The

features can be lags, transformations on the lags and date features. You

can also define transformations to apply to the target before fitting,

which will be restored when predicting.

from mlforecast import MLForecast

from mlforecast.lag_transforms import ExpandingMean, RollingMean

from mlforecast.target_transforms import Differencesfcst = MLForecast(

models=models,

freq='D',

lags=[7, 14],

lag_transforms={

1: [ExpandingMean()],

7: [RollingMean(window_size=28)]

},

date_features=['dayofweek'],

target_transforms=[Differences([1])],

)To compute the features and train the models call fit on your

Forecast object.

fcst.fit(series)MLForecast(models=[LGBMRegressor, LinearRegression], freq=D, lag_features=['lag7', 'lag14', 'expanding_mean_lag1', 'rolling_mean_lag7_window_size28'], date_features=['dayofweek'], num_threads=1)

To get the forecasts for the next n days call predict(n) on the

forecast object. This will automatically handle the updates required by

the features using a recursive strategy.

predictions = fcst.predict(14)

predictions| unique_id | ds | LGBMRegressor | LinearRegression | |

|---|---|---|---|---|

| 0 | id_00 | 2000-04-04 | 299.923771 | 311.432371 |

| 1 | id_00 | 2000-04-05 | 365.424147 | 379.466214 |

| 2 | id_00 | 2000-04-06 | 432.562441 | 460.234028 |

| 3 | id_00 | 2000-04-07 | 495.628000 | 524.278924 |

| 4 | id_00 | 2000-04-08 | 60.786223 | 79.828767 |

| ... | ... | ... | ... | ... |

| 275 | id_19 | 2000-03-23 | 36.266780 | 28.333215 |

| 276 | id_19 | 2000-03-24 | 44.370984 | 33.368228 |

| 277 | id_19 | 2000-03-25 | 50.746222 | 38.613001 |

| 278 | id_19 | 2000-03-26 | 58.906524 | 43.447398 |

| 279 | id_19 | 2000-03-27 | 63.073949 | 48.666783 |

280 rows × 4 columns

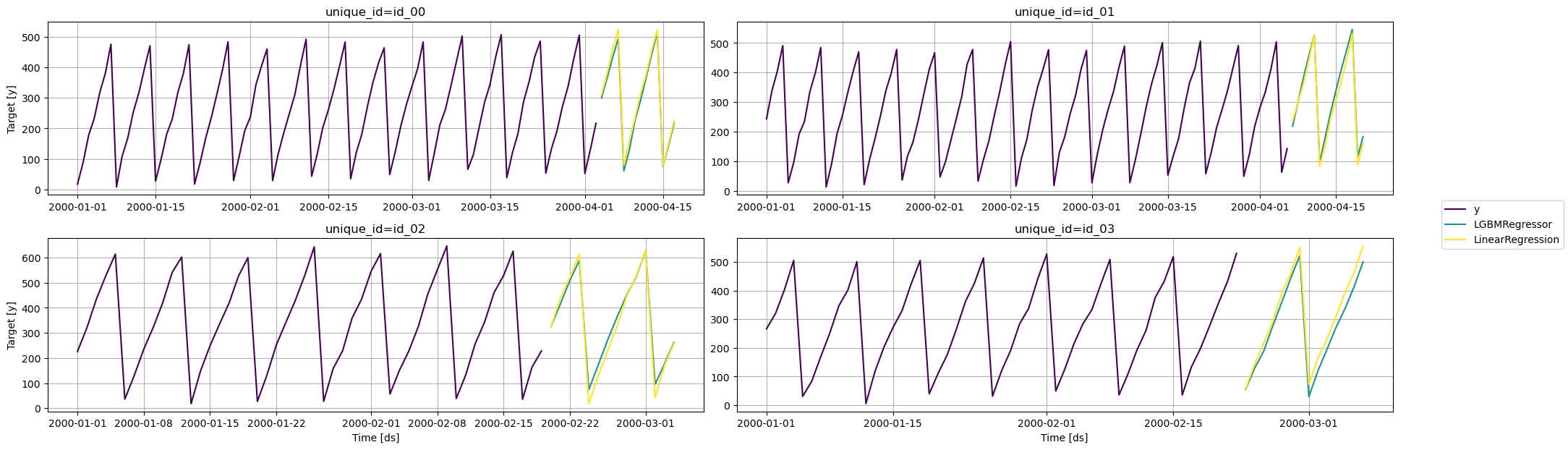

from utilsforecast.plotting import plot_seriesfig = plot_series(series, predictions, max_ids=4, plot_random=False)

See CONTRIBUTING.md.

![dependabot[bot] avatar](https://avatars.githubusercontent.com/in/29110?v=4 "dependabot[bot]")